The Delayed Scan: What PayPal’s Integration with WeChat Tells Us About the Impossible Trinity of Great-Power Finance

Behind the scenes of WeChat Pay’s new cross-border compatibility: The micro-concessions and macro-anxieties of RMB internationalization.

The financial isolation of international tourists grappling with China’s cashless economy has finally seen a glimmer of policy loosening. According to recent reports, WeChat Pay has begun allowing foreign visitors to link and use their PayPal accounts directly for domestic QR-code transactions.

While undeniably a massive boon for global travelers, anyone with a passing understanding of financial technology will likely ask the same fundamental question: What took so long?

Technically speaking, integrating PayPal into WeChat Pay is a minor task that a single Tencent software engineer could wrap up over a single night of overtime.

This multi-year delay was never an issue of technical incompatibility or a petty dispute over corporate margins. It was a silent, protracted chess match over monetary sovereignty, capital controls, and national financial security.

I. “The Musk Question” and the Obsession with Financial Risk

To understand Beijing’s deep-seated caution toward opening its micro-payment ecosystem to foreign players, one must first confront the historical trajectory of domestic fintech regulation. In November 2020, during the crisp autumn weeks when Ant Group’s mammoth IPO was abruptly mothballed, China’s most prominent celebrity entrepreneur vanished from the public eye. By September 2021, as his prolonged absence fueled global speculation, it culminated in the famous, blunt query Elon Musk threw at the international tech community: “Where is Jack Ma?”

From a hard-nosed macroeconomic perspective, this historical turning point was a textbook conflict over credit creation. On the eve of its aborted listing, Ant Group was leveraging a modest base of proprietary capital to anchor trillions of yuan in co-originated loans through the relentless securitization (ABS) of its credit assets.

In the analytical frameworks of the Chicago School on private liquidity generation and Hyman Minsky’s “Financial Instability Hypothesis,” this model was effectively creating systemic fiat liquidity while bypassing the capital-adequacy guardrails of the Basel Accords. When a private tech giant begins to encroach upon the ultimate prerogative of a central bank—the monopoly over liquidity generation—the leadership in Beijing did not hear the music of innovation; they heard the echo of the 1997 Asian Financial Crisis and the 2008 Wall Street crash.

Nobel laureate Joseph Stiglitz, in his autopsy of the 1997 East Asian collapse, argued cogently that opening up capital accounts rapidly without deep institutional regulations and robust firewalls is catastrophic for developing states. The institutional memory China walked away with from those crises is clear: micro-level efficiency and technological convenience can rapidly morph into a financial contagion superhighway during moments of systemic panic. The ultimate answer to Musk’s query lies here—to avert systemic risk, the emergency brakes will be slammed on any private financial innovation that tests the red lines of state oversight.

II. The Great-Power Impossible Trinity and the Sacrifices of the “World’s Factory”

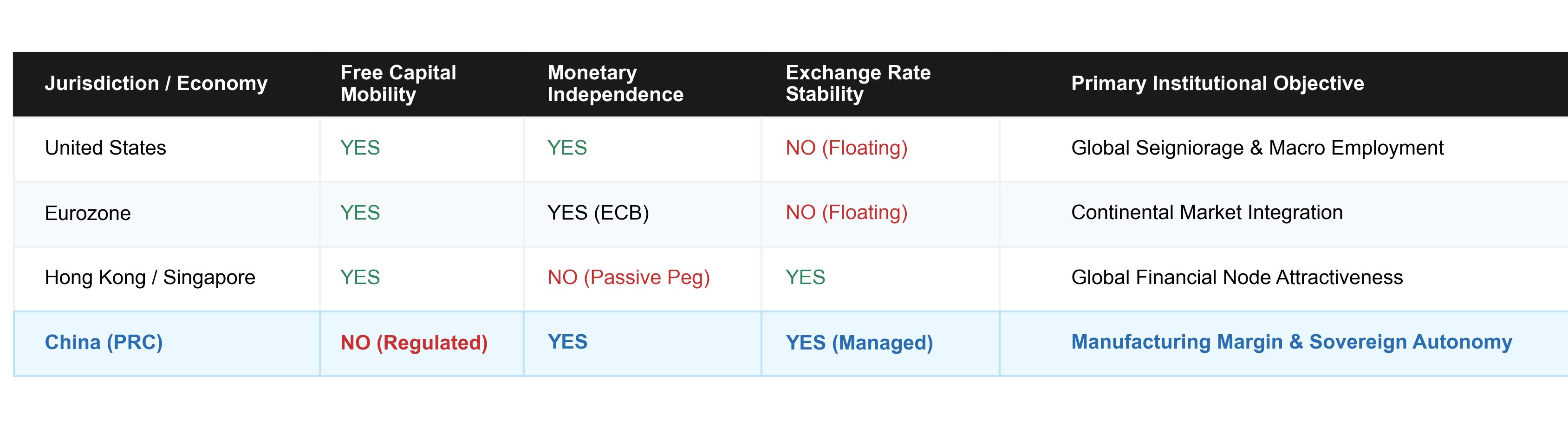

This strict posture toward financial preservation translates directly into the cross-border arena through the absolute mathematical law of Paul Krugman and Robert Mundell’s “Impossible Trinity” (The Trilemma).

The theorem posits that a sovereign economy can choose only two of the following three policy objectives:

Free Capital Mobility

Independent Monetary Policy

Exchange Rate Stability

This reality forces a stark institutional divergence between vast continent-sized states and smaller hubs. Highly concentrated island or city-state economies like Hong Kong or Singapore opt for exchange rate stability and free capital mobility to anchor their status as global financial nodes. In doing so, they consciously surrender an independent monetary policy (when the Federal Reserve hikes interest rates, Hong Kong must passively mimic those moves, regardless of local economic bleeding).

But no superpower can afford to yield its monetary policy independence—the primary lever for managing domestic employment, curbing inflation, and stabilizing macroeconomic performance. This is doubly true for China, a nation possessing an intense sense of historical pride, a deep-seated consciousness of its geopolitical destiny, distinct ideological mandates, and an unyielding mission to assert itself as a peer superpower. A state character of this nature will never delegate the pricing of its foundational economic livelihood to external market forces. Simultaneously, as the definitive “world’s factory,” China fundamentally requires a predictable exchange rate to protect the margins of its massive manufacturing and export base.

Trapped by the iron logic of the Trilemma, having locked in monetary independence and exchange rate stability, Beijing must sacrifice free capital mobility. If foreign card networks and global payment behemoths were permitted to seamlessly tap into the everyday consumer arteries of the domestic economy, China’s massive current account surpluses and manufacturing wealth would face unprecedented flight pressures during Federal Reserve tightening cycles. A major sovereign state cannot survive that level of bloodletting. Consequently, enforcing strict micro-barriers—such as engineering UnionPay to isolate Visa and Mastercard, or capping individual cross-border capital access at $50,000 annually—remains a reactive but necessary cost of preserving sovereign autonomy.

III. The Triffin Dilemma Variant: The Structural Deadlock of RMB Internationalization

This strategic friction—the desire for global monetary prestige matched by a profound fear of losing domestic control—has cornered the internationalization of the RMB into a conceptual deadlock.

In official macro narratives, elevating the RMB to a global currency is a deeply alluring geopolitical project. It promises substantial seigniorage windfalls and functions as a formidable geopolitical lever. By offering RMB-denominated credit lines and swap clearings to developing economies and commodity exporters caught between the two global poles, Beijing can anchor these states firmly within its sphere of influence. Furthermore, it constructs a defensive trench against the threat of SWIFT-based financial sanctions in the event of severe geopolitical conflict.

Yet, as the economist Eswar Prasad notes, Beijing is attempting a historical anomaly: creating a global reserve currency without a fully open capital account. This runs headfirst into a modern variant of the classic Triffin Dilemma. To supply the world with global liquidity, a nation must run chronic trade deficits; more critically, its currency must become a “decentralized, free asset”—one that global hedge funds, speculators, and asset managers can freely borrow, short, hedge, and trade at will.

The baseline vulnerability of China’s top-down corporate and banking balance sheets means it cannot tolerate that degree of market exposure. Raising the floodgates would leave its massive internal domestic asset valuations directly naked to the predatory currents of global capital.

As a consequence, a powerful, clear-eyed, and deliberate institutional force continues to constrain the RMB at the micro-level, rendering its cross-border velocity intentionally sluggish. The “internationalization” of the currency is thus strictly quarantined within state-directed macro pipelines: bilateral central bank swaps, sovereign strategic investments, and government-brokered commodity invoicing. The data looks magnificent on state ledgers, but in the micro-world of everyday transactions—and on the screens of international tourists—the currency remains highly localized, ring-fenced, and structurally inhibited.

Conclusion: A Managed Sandbox

Why, then, has this policy shift finally occurred now?

Amidst high-level diplomatic negotiations and structural bargaining between the two superpowers, access to core financial sectors is slowly grinding forward. However, this is not a traditional pivot toward free-market liberalism; it is a classic case of “marginal institutional change” within institutional economics—where the boundaries move only when the marginal benefits outweigh the systemic risks.

The integration of PayPal into WeChat Pay is meticulously cordoned within a highly controlled “regulatory sandbox” designed strictly for unidirectional capital inflows. International travelers spend foreign currency held in external accounts, while Tencent and designated domestic clearing banks handle the backend foreign exchange netting and settle with local merchants in yuan. The transaction offers seamless utility to the traveler on the ground, yet at the macro level, the volume, direction, and purpose (restricted entirely to domestic retail consumption) remain one hundred percent transparent, auditable, and trace-heavy.

The state’s financial defense apparatus yields none of its core monetary sovereignty and incurs zero capital flight risk, yet it successfully captures the tangible economic dividend of foreign consumer spending.

This newfound cross-border compatibility is not a celebratory overture for the liberalization of the RMB; it is another masterfully executed exercise in China’s doctrine of “managed access.” Before this towering firewall of financial security, true internationalization remains a carefully choreographed, heavily monitored dance in chains.

As a final observation: in the grand narrative of digital convenience, WeChat Pay and Alipay have always operated as inseparable twins. Yet, this recent breakthrough spotlighted Tencent alone, leaving Alibaba conspicuously absent from the frame. One cannot help but indulge in a bit of dry humor: has Jack Ma, despite practicing the art of quiet invisibility for so many years, still not completely secured a full measure of institutional absolution?